Many seniors share a similar goal for their later years: a retirement filled with security, independence, and the freedom to enjoy time without constant worry. We plan for routine doctor visits and monthly bills, but few budget for a sudden misstep that changes everything. A fall is often viewed purely as a medical crisis, yet for many older adults, it quickly becomes a financial emergency that threatens hard-won stability.

The economic landscape for older adults is already shifting. With news that seniors on Social Security could face a potential $460 monthly cut to benefits if legislative action isn't taken, financial margins are tighter than ever. Furthermore, up to 80% of older households are currently considered economically insecure or at risk of falling into poverty due to rising costs for basics like housing and healthcare. In this climate, the cascading costs of a fall can deplete retirement savings. This guide provides a clear look at the real price of these incidents and offers a practical plan for preparation and recovery.

What Are the Real Financial Costs of a Senior Fall?

When we think of a fall, we might picture a bruise or a sprain. However, the financial reality is much starker. The total medical costs associated with fall injuries for older adults have ballooned to approximately $50 billion annually. Understanding where this money goes is the first step in protecting your finances.

Immediate Medical Bills and Medicare Gaps

Expenses begin accumulating the moment an ambulance is called. Each year, approximately 3 million older adults are treated in emergency departments for fall injuries. These visits trigger copays, deductibles, and facility fees that can pile up instantly. While Medicare is a lifeline, it does not cover every expense incurred during a crisis.

Many seniors are surprised to face out-of-pocket costs for services not deemed "medically necessary" by insurers or for extended hospital stays. This is particularly common with severe injuries like hip fractures. More than 95% of hip fractures occur as a result of falls, most commonly when a person falls sideways. These injuries almost always require surgery and hospitalization, pushing the limits of standard coverage and dipping into personal savings.

The Long Road to Recovery: Ongoing Expenses

The initial hospital bill is often just the deposit on a much larger total. Over a third of falls result in a serious injury, such as broken bones or a head injury, which demands extensive long-term care. Recovery is rarely a straight line, and the costs can persist for months or even years.

You may find yourself paying for a variety of recurring needs that insurance covers only partially or not at all. Such hidden expenses may include the following:

- Physical and Occupational Therapy: Copays for sessions needed two to three times a week can add up quickly.

- Prescription Medications: Pain management and bone-strengthening drugs often come with significant tier-based copays.

- Durable Medical Equipment: Items like walkers, wheelchairs, or hospital beds for home use.

- In-Home Health Aides: Non-medical care, such as help with bathing or cooking, is rarely covered by traditional Medicare.

- Specialist Follow-ups: Frequent visits to orthopedists or neurologists.

Home and Lifestyle Modifications

Returning home after a fall often means spending money to make that home safe again. You might need to install grab bars, build wheelchair ramps, or add stairlifts. In 2025, the senior housing sector saw valuations recover and occupancy rise, but for those wishing to age in place, utilizing home equity is becoming a key strategy to fund these renovations.

If staying home isn't possible, the alternative is costly. The death rates from falls for adults aged 85 and older more than doubled between 2003 and 2023, highlighting the severity of the risk for the oldest among us. This increasing risk often forces families to consider assisted living, where expenses are high and rising due to inflation and labor shortages.

How Can You Financially Prepare for a Potential Fall?

Waiting until an accident happens is the most expensive way to manage a fall. By taking steps now, you can build a financial and physical safety net that protects your future.

Reviewing Your Health Insurance Coverage Now

It is vital to review your insurance policies before a crisis strikes. Medicare, Medigap, and Medicare Advantage plans vary significantly in how they handle skilled nursing facilities and rehabilitation. With senior care bankruptcies rising by 18% recently, the stability of some care providers is in flux, making it even more important to know exactly what your plan guarantees. Ask your provider specifically about "custodial care" coverage, as this is the biggest gap for most seniors recovering at home.

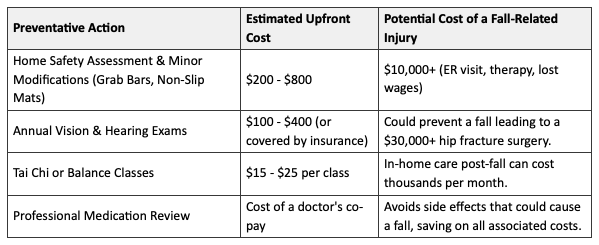

Prevention as Your Best Financial Strategy

Think of fall prevention as an investment strategy. Every dollar spent on safety is thousands saved in medical bills. New research highlights that prevention goes beyond just watching your step; for instance, nighttime sleep duration is significantly correlated with an increased risk of falls among older adults. Addressing sleep issues is a low-cost medical intervention that reduces high-cost risks.

Technology is also shifting the focus from reaction to prevention. Innovative monitoring tools are now helping identify warning signs of decline before a fall occurs, potentially saving the healthcare system and families billions. Investing in these preventative measures is far cheaper than the alternative.

What to Do When Negligence Causes a Fall?

Sometimes, a fall is not caused by frailty or a simple mistake, but by a hazardous condition that should have been fixed. In these cases, your financial recovery plan involves understanding your legal rights.

Identifying a Potentially Liable Party

Property owners, whether they run a grocery store or manage an apartment complex, have a legal responsibility to keep their premises reasonably safe. If you tripped over a broken sidewalk, slipped on an uncleaned spill, or fell due to poor lighting, negligence may be at play. Financial settlements for these incidents can be critical for covering medical debts.

Your Right to Financial Recovery

If your injury was caused by someone else's carelessness, you shouldn't have to drain your retirement savings to pay for it. You may be entitled to compensation for your medical bills, ongoing therapy costs, and pain and suffering. Navigating an insurance claim or legal process while recovering can feel impossible. For those who are unsure what to do after a slip and fall accident, getting expert guidance is a crucial step. Seeking a free consultation with a compassionate legal team can provide clarity on your rights and help you pursue the compensation needed to cover these devastating, unplanned expenses. This allows you and your family to focus on what truly matters: healing.

Steps to Take to Protect Your Rights

Taking the right actions immediately after an incident can make or break your ability to recover costs. If you are physically able, report the accident to a manager or landlord right away. Take clear photos of the hazard that caused your fall and gather contact information from any witnesses. Finally, seek medical attention immediately to document your injuries. This documentation reinforces the advice in our A Guide on What to Do After a Fall on Concrete and serves as vital evidence if you need to file a claim.

Preserving Your Health and Financial Well-Being

A fall can change life in an instant, but it doesn't have to ruin your financial future. While the statistics are sobering—more than 41,000 Americans aged 65 and older died as a result of a fall in 2023—being informed is essential. By understanding the hidden costs, investing in prevention, and knowing your rights regarding negligence, you can build a robust defense. You have worked hard for your independence; taking these practical steps helps ensure you keep it.

Image generated by Gemini